Mortgages may seem daunting to the uninitiated, but in reality, they’re pretty straightforward. The basic premise of a mortgage is taking out a loan to purchase a home and within this premise, there are many paths to take to home ownership. Today, we’ll look at these different paths as we’ll cover the different types of mortgages that are out there to choose from. It’s also worth advising to use a trusted mortgage broker when looking for your home loan, as there are many different loan types available and it can be daunting trying to deal with all the banks and lenders.

Jumbo Mortgage

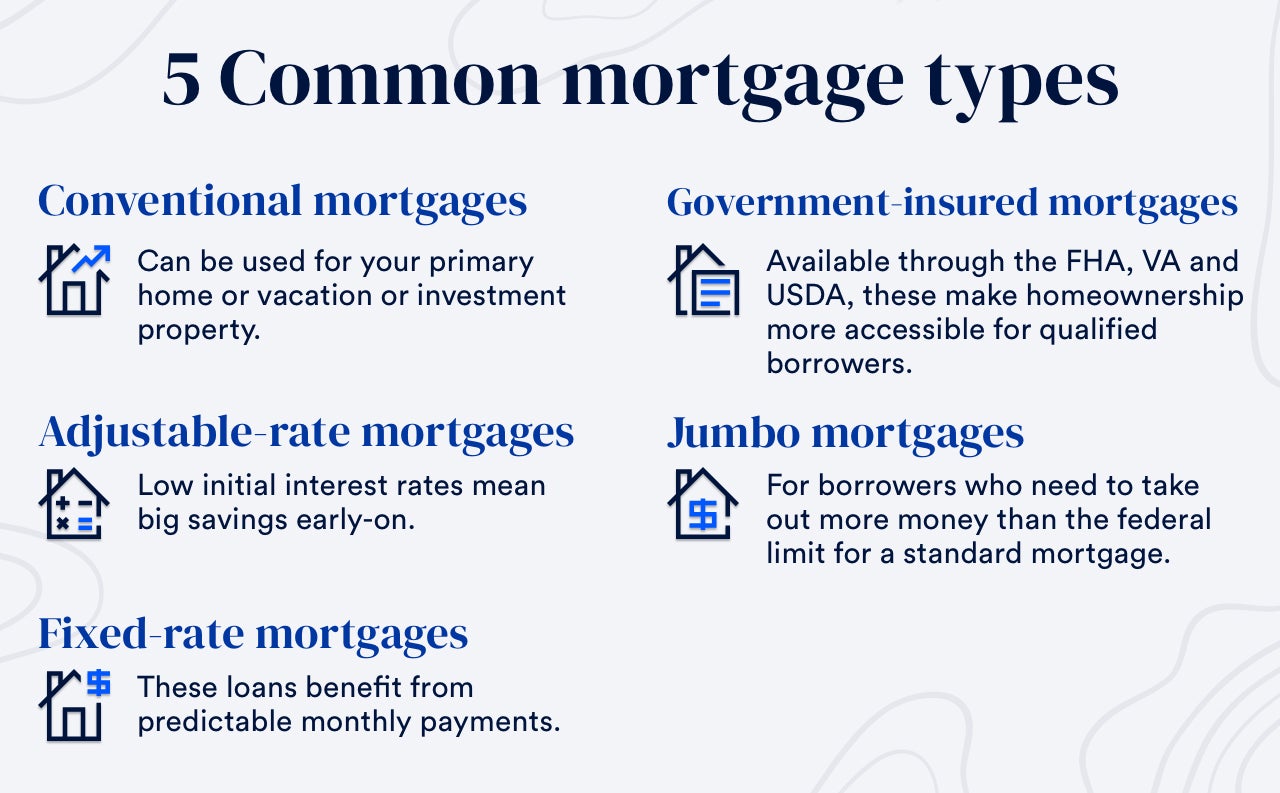

As the name implies, jumbo mortgages are high-ticket item mortgages geared toward expensive properties. The loan term APR rates can either be fixed or adjustable and have special terms to qualify for the mortgage. Borrowers must have a credit score of 700 or higher and are also required to have at least 10% down payment on the property.

VA Mortgage

VA Mortgages are backed by the Department of Veterans Affairs and this kind of mortgage is perfect for veterans of the armed forces. These mortgages offer veterans special low-interest rates and no down payment required to establish home ownership. Veterans just out of the service and looking to buy a home should look into these kind of mortgages as they can save quite a bit of money over the long term.

Interest-Only Mortgage

Interest-only mortgages are very unique as the borrower only pays on the interest of the note with their monthly payments. It’s up to the borrower to make payments on the principal of the note separately. This kind of mortgage is perfect for those not planning to spend a lot of time in the property.

USDA Mortgage

USDA Mortgages are mortgages backed by the United States Department of Agriculture and were originally geared towards farms and other rural properties. No down payments are required on most USDA mortgages and you can apply for improvements to the property over time with this mortgage.

Adjustable-Rate Mortgage

Adjustable rate mortgages or ARM’s as they’re usually called are a special kind of mortgage. The usual process in an ARM is to have an introductory APR upon the start of the note. This introductory low APR rate is locked in for a set amount of time. This period can last anywhere from one to ten years depending on the lender. Once this introductory period ends, the rate is adjusted according to the Prime Rate. If the Prime Rate rises, then your APR will rise as well and vice versa if the Prime Rate drops. This kind of a mortgage can be a bit of a gamble as you can end up with some nice interest rates if the Prime Rate goes through a down period. Conversely, you could also end up with a horrible loan rate for a period as well. If necessary, read further on ARM vs a fixed-rate loans.

FHA Mortgage

FHA mortgages or Federal Housing Administration mortgages are geared for lower-income borrowers. These loans have special provisos that lower-income borrowers can use to qualify for an FHA loan. These provisos include borrowers with credit scores as low as 500 and borrowers can be allowed to have a very low down payment, in some cases below 5%. The downside with such a low barrier of entry is the fact that you’ll be paying PMI on the monthly payments until you establish 20% equity in the home. This kind of mortgage can be a lifechanger for those with low credit scores and not much money to establish a down payment.

15-Year Fixed-Rate Mortgage

The 15-year fixed-rate mortgage offers a lower APR rate in comparison to other popular kinds of mortgage. The only sticking point of this kind of mortgage is the higher monthly payments affixed to a loan like this. The higher payments make sense when you consider the normal range of a 30-year loan monthly payment. You’re in essence, condensing a 30-year note into half the time with a 15-year note, so naturally the payments will reflect that. This particular kind of mortgage is the go-to when you’re refinancing your original mortgage. This kind of mortgage would be ideal for those who have the income to support the higher monthly payments as you end up paying much less interest over those 15 years versus a standard 30-year note.

30-Year Fixed Rate Mortgage

We’ve saved the most popular option for last, the venerable 30-year fixed-rate mortgage. This kind of mortgage is the most popular for a good reason and that’s due to the length of time allotted and the low cost of the monthly payments. This kind of mortgage is the lowest-entry point for most of us out there. The usual route is to have 20% down payment to get out of PMI (Private Mortgage Insurance) status and enjoy the predicability of having a low monthly payment for a long period of time. The APR on the note will not change with the Prime Rate as it’s a fixed-rate mortgage.